Every homeowner will eventually reach a point where they will ask themselves, “If I was to remodel my kitchen, would I Do-it-Myself or get a Kitchen-as-a-Service?”

With a Swedish kitchen remodel offering organized bliss and respectable prices… the extra labor often gets lost among the endless supply of nuts, bolts and Allen wrenches. Left to wonder how an entire kitchen will fit into a hatch-back, another big-box store promises to not only deliver… but also design, install, and finish the project. While both will support the kitchen sink, homeowners everywhere are left to weigh the merits of Scandinavian design against the ‘one-and-done’ approach.

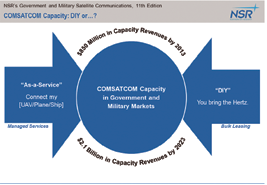

Similarly, Government and Military (MAG) end-users must make a choice when procuring Commercial Satellite Capacity (COMSATCOM), “Do I get the Hertz myself, or Get-it-as-a-Service?” Mainly, do they go the bulk leasing route, which offers cheaper per-MHz pricing and more flexibility at the cost of ‘some assembly required’, or the Managed Services direction that offers full-service, tailored solutions/applications at a potentially higher cost?

Just as every homeowner will reach that crossroad, the U.S. Government has found that ‘DIY’ vs. ‘As-a-Service’ depends on the situation. Specifically, all depends on the demands on the ground, the supply of proprietary capacity available in space, the technical abilities of the organization procuring the capacity (and security requirements), and the timeline over which the capacity will be used… plus the available budget. For the U.S. Government, Bulk Leasing has long been the popular choice when demands exceeded proprietary supply, taking advantage of the flexibility of raw capacity.

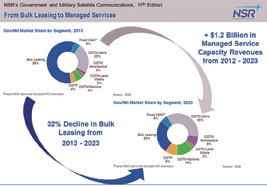

NSR’s recently released Government and Military Satellite Communications, 11th Edition study found that bulk leasing contracts contributed 58 percent of MAG Satellite capacity revenues in 2013. Yet, over the past few years, managed services have become more attractive—both in the U.S. and around the world. Looking forward, that trend will only intensify with bulk leasing expected to contribute only 26 percent of MAG Satellite capacity revenues by 2023. In dollars, it will grow by just over $50 million, compared to $1.2 billion for managed services from 2013 to 2023, a clear shift in market direction.

Why, then, if the DIY route has provided value and flexibility for years, are MAG end-users opting for the ‘As-a-Service’ offering? The drivers of this change are two-fold: cost and capability.

As homeowners seldom include the cost of renting a larger car and the tools/training required to assemble the cabinets, counters, plumbing, and appliances into the cost of their ’DIY’ kitchen, government end-users have found that the “Do-it-yourself” aspect of satellite

capacity can strain budgets and complicate operations. By consolidating the many disparate elements of coordinating a networked service into a single external contract, managed services can provide a more cost effective solution than bulk leasing and internal network management.

Further, as demands for satellite capacity increase, uses of satellite connectivity become more complicated and greater expertise to establish and manage networks is required, it is increasingly attractive for the entire process to be outsourced through a managed service contract. This contract draws on expertise and solutions already developed and refined through industry experience. The ‘As-a-service’ solution through managed services procurement can contribute new capabilities to the overall system without requiring development investment by MAG players.

Even when the necessary capabilities in manpower and technology do exist, the reallocation of resources to manage the network in-house is not always justified by the gain in network control and flexibility. The dynamics of MAG SATCOM has now morphed toward application centric thinking. This makes the question, “How many meatballs do I want,” rather than, “what size Allen wrench do I need (and then learning about kitchen design theory)?” Managed services that provide integrated solutions with fewer moving parts streamline procurement, and NSR expects new services (such as UAVs) to opt for these solutions as they are rolled out.

The homeowners have already seen the shift—you can now have your Scandinavian kitchen without lifting a single tool.

MAG markets are in the middle of this transition, with providers moving further down the value-chain, consolidating offerings, and similar to kitchens, focusing on how people will use capacity. HTS will only further accelerate this shift. With a greater focus on delivering maritime mobility, serving UAV platforms, or supporting highly-mobile armed forces, the role of the Managed Services will be a go-to solution across the MAG markets.

However, there will always be users with a love of ‘DIY.’ For them, this model of Bulk Leasing some X-band, MEO-HTS, and Ka-band capacity (while still, maybe, getting the ‘countertop-as-service’) will be how they support their requirements.

Changing fiscal and technical landscapes are driving MAG users away from the DIY bulk leasing to the “Kitchen-as-a-Service” Managed Service model. With emerging programs such as U.S.A.F.’s Pathfinder, bulk leasing will not go away. However, an overwhelming share of growth over the next decade will be from Managed Services connecting Aeronautical, UAV, and Maritime SATCOM terminals on C-, Ku-, Ka-, X- and GEO/MEO-HTS networks.

Overall, service providers and satellite operators will need to work on the right mix of “do-it-yourself”, and “as-a-service” to capture this market potential.

Mr. Grady has been involved in the Satellite Communications industry since 2005, joining NSR in 2010. He is NSR’s Energy market subject matter expert, and a core member of NSR’s mobility research practice for both civil and government markets. He regularly provides his insights and analysis to NSR’s single-client consulting practice, and is also a regular contributor to leading industry publications and forums.

Before joining NSR, Mr. Grady served as the Sustainable Development Projects Coordinator Intern with the Global VSAT Forum where he worked regularly with the GVF Secretariat and the Regulatory Working Group on many of the forum’s initiatives. Working with the Regulatory Working Group, Mr. Grady helped develop and implement various RWG initiatives aimed at protecting satellite spectrum, increasing awareness of satellite services, and working to promote regulatory reforms across the globe. He works in NSR’s Washington DC office.